Europe pushes back its zero-emission commercial vehicle targets: What this means for European OEMs and the transition to sustainable CV transportation

By Luke Willetts - 1st April 2025

European truck OEMs

Belgium – Last month, we explored the impact of a potential Trump 2.0 administration on the U.S. zero-emission Commercial Vehicle (CV) industry. This month, our focus shifts to Europe, where the European Union (EU) has rolled back its CO₂ targets. Initially, these regulations mandated that OEMs meet strict EV sales benchmarks by 2025. However, under pressure from automakers and lobbying groups like the Brussels-based European Automobile Manufacturers’ Association (ACEA*), the EU has softened its stance, acknowledging concerns that the original targets were unrealistic and could hinder Europe's global competitiveness.

Revised Targets and Extended Compliance Period

The European Commission has extended the compliance period for the 2025 emission targets from one year to three years. This extension, though unsurprising, is a response to multiple factors, including a downturn in the German automotive industry, the rise of Chinese CV EV capabilities, and the uncertainty surrounding Trump-era tariffs. OEMs now have until 2028 to meet the 2025 CO₂ reduction targets. While this allows manufacturers additional time for compliance, environmental organisations and the public have criticised the move, arguing it delays the transition to zero-emission vehicles, scheduled for 2035. Manufacturers, on the other hand, see this as a necessary reprieve that offers flexibility and reduces immediate financial pressure associated with non-compliance penalties.

Euro VII: Stricter Emission Regulations and Rising Costs

European OEMs are facing regulatory pressures to sell more zero-emission CVs while simultaneously upgrading ICE engines to meet the stringent Euro VII legislation. Euro VII consolidates regulations for cars, vans, and heavy-duty vehicles under a single framework. While it retains the Euro 6 emissions limits for cars and vans, it significantly lowers the limits for buses and trucks. Additionally, it introduces restrictions on brake dust and tyre particles, pushing OEMs to accelerate the adoption of regenerative braking technology.

European Commission

Beyond gas emissions, Euro VII mandates battery durability limits, onboard emissions monitoring systems, and new pollutant restrictions, including ammonia, formaldehyde, and nitrous oxide (N₂O). The European Commission estimates that the cost of compliance for new trucks and buses will rise by EUR 2,700 per vehicle—a concerning figure given the competitive pricing of Chinese manufacturers. The EC justifies these costs by citing the estimated environmental benefits, which outweigh costs by a ratio of more than five to one. Furthermore, the legislation introduces new battery durability standards for electric vehicles and mandates that plug-in hybrids switch to electric-only mode in designated city centres.

For OEMs, these regulations translate into increased costs, technical challenges, and market uncertainties. The need for substantial investments in R&D, advanced exhaust treatment systems, and compliance measures may impact fuel efficiency and vehicle performance, adding further complexity to an already challenging regulatory landscape.

DAF assembly line in Eindhoven factory

ACEA’s Concerns: Infrastructure and Government Funding

ACEA has repeatedly highlighted the lack of critical infrastructure and government funding for alternative power sources. The organisation argues that Euro VII will divert capital investment toward cleaner ICE CVs at the expense of electrification. ACEA’s calculations suggest that achieving a 45% CO₂ reduction target by 2030 requires at least 50,000 publicly accessible chargers and 700 hydrogen refuelling stations, with an estimated transition cost of USD 50–60 billion, according to the World Economic Forum (WEF).

ACEA truck manufacturers agree that both hydrogen-powered and battery-electric trucks will play a pivotal role in the future of green transportation. While some OEMs prioritise battery-electric vehicles, others invest in hydrogen fuel cell technology and LNG solutions. ACEA also emphasises the ongoing relevance of fossil-free fuels like biofuels, biogas, and green hydrogen in the transition to climate neutrality. However, infrastructure remains the key bottleneck, as Europe currently lacks sufficient public charging and refuelling stations, particularly for electric and hydrogen trucks. Even truck-specific filling stations for natural gas (CNG and LNG) remain scarce across the continent.

Industry leaders meet at the ACEA HQ in Brussels, earlier this year

Publicly Funded Infrastructure Projects

Beyond charging and refuelling stations, infrastructure development also involves the production of green energy suitable for heavy-duty vehicles. Christian Levin, CEO of Scania, has stressed the need for specialized high-power charging infrastructure for commercial vehicles, with at least a one-megawatt power output to meet demand.

To address this, the European Parliament passed the Alternative Fuels and Infrastructure Regulation Act in July 2023. This legislation mandates that high-power charging stations (1,400–2,800 kW) be installed every 120 km along major highways by 2028, with hydrogen refuelling stations required every 200 km by 2031. Member states must commit to a mandatory minimum infrastructure target and submit roadmaps to the European Commission. The Alternative Fuels Infrastructure bill has a budget of EUR 1 billion.

Mercedes-Benz truck charging station in Wörth am Rhein, Germany

This year, the EU awarded nearly EUR 422 million in grants to 39 projects via the Connecting Europe Facility, funding 4,900 electric charging points and alternative fuel stations. The European Commission has also approved EUR 1.4 billion in public funding for hydrogen-related projects under the ‘Hy2Move’ initiative, involving major companies such as Airbus, Air Products, BMW, and Michelin. These projects, expected to unlock an additional EUR 3.3 billion in investments, will contribute to hydrogen production, storage, and transport applications across Europe.

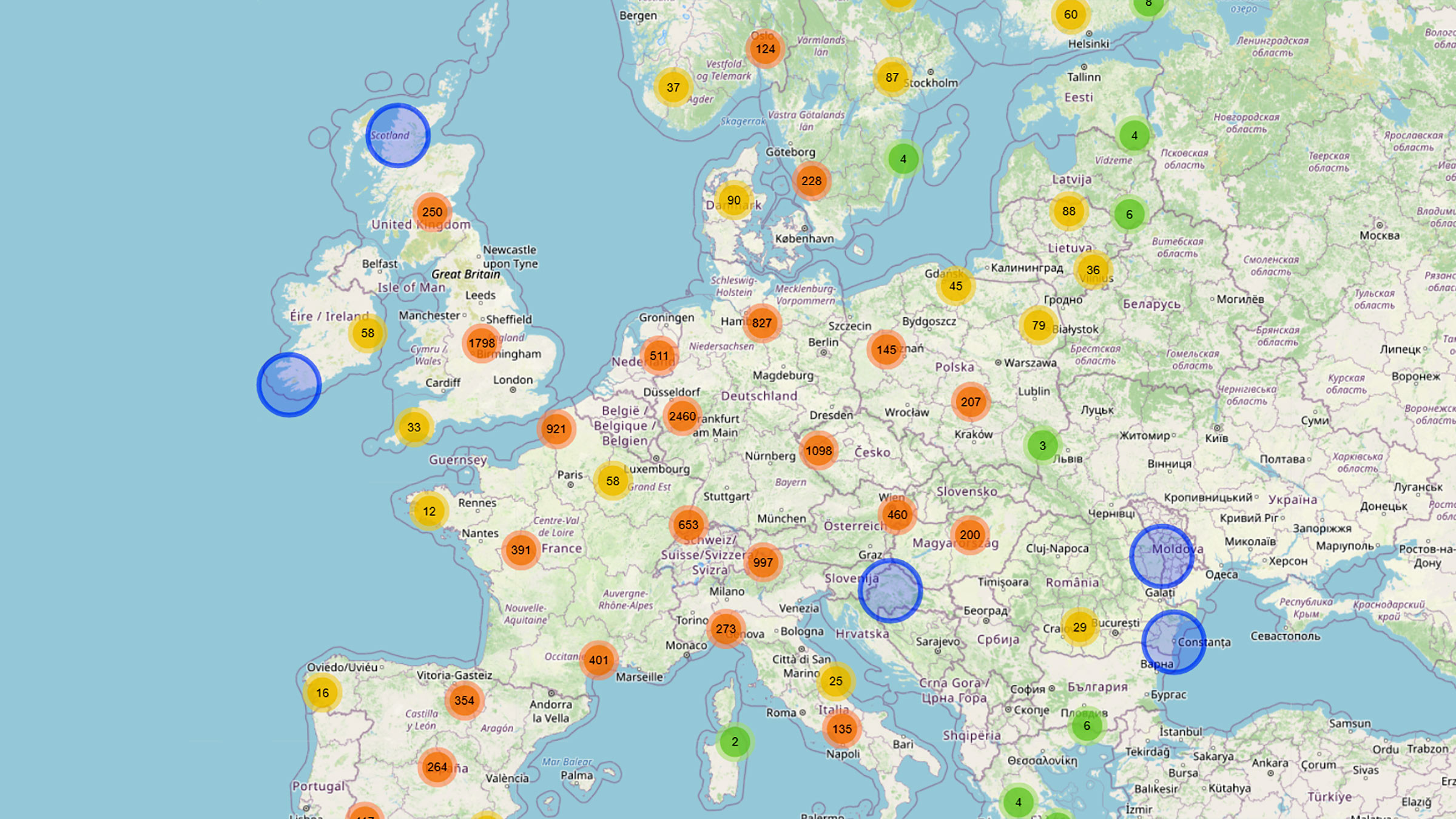

ACEA map of priority points for e-truck charging stations

Private Sector Infrastructure Development

In the private sector, a charging infrastructure joint venture (JV) between Traton SE, Daimler Truck AG, and AB Volvo called Milence plans to install and operate at least 1,700 charging points supplied with renewable energy on highways and at logistics hubs across Europe. Initially proposed in 2021, the JV has received regulatory approvals and in 2022 appointed a CEO, Anja van Niersen. Each company has committed to investing EUR 500 million, intending to encourage greater and swifter uptake of electric vehicles in Europe. In January 2024, Milence opened its first charging facility in the Netherlands. The company has since opened charging stations in France, Germany, Belgium and most recently, the UK.

Milence charging hub in Immingham, UK

BP Pulse is also investing heavily in Europe’s EV infrastructure, planning ultra-rapid charging corridors for electric HGVs. Meanwhile, companies like ChargePoint and Kempower have demonstrated megawatt charging prototypes, though grid management remains a concern, especially in towns/cities where grid capacity is already stretched. This will also require costly circuit infrastructure to handle drawing large quantities of electricity from the grid. Who will fit the bill?

Kempower megawatt charger

The Current State of the European CV Market

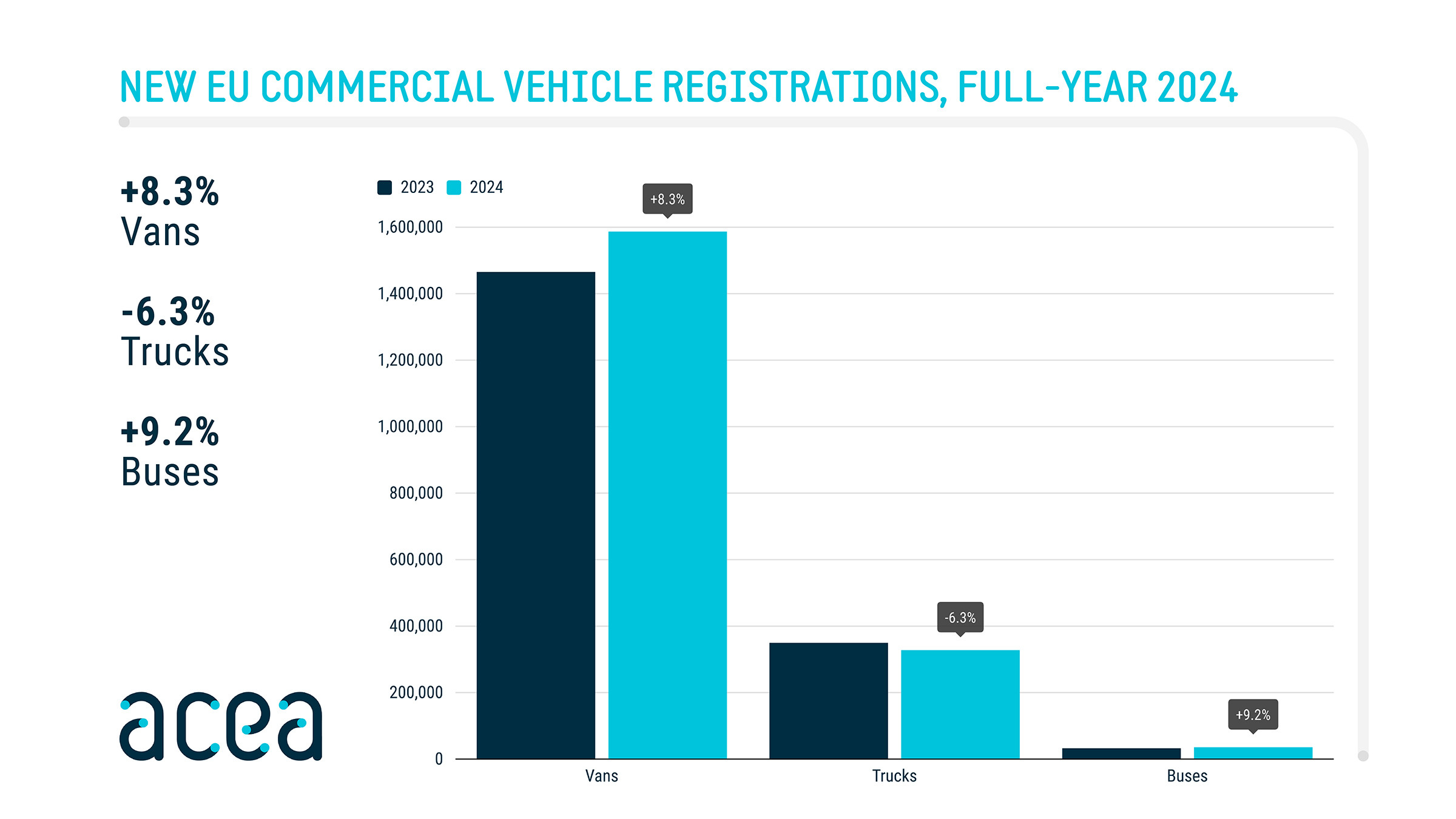

Despite these efforts, the electric truck market has struggled to gain traction. According to 2024 ACEA data, new truck registrations fell by 6.3%, driven by an 8.5% drop in HGV sales. Diesel-powered trucks still dominate, accounting for 95.1% of new registrations, while electric truck sales stagnated at 2.3%.

By contrast, the EU bus market grew by 9.2%, with electric bus registrations rising by 26.8%, driven largely by growth in Italy and Spain. Meanwhile, hybrid-electric bus sales declined, and diesel bus registrations increased. The EU van market also experienced growth, with diesel vans still making up 84.5% of sales, while electric van market share declined from 7.2% to 6.1%.

EU CV Sales in 2024

The EU Commission’s Action Plan

On March 5, Ursula von der Leyen unveiled the Industrial Action Plan for the European Automotive Sector, focusing on competitiveness, sustainability, and innovation. The plan allocates EUR 2.2 billion for charging infrastructure expansion and EUR 1.8 billion for securing raw materials for battery production. However, critics argue that its emphasis on battery-electric technology overlooks hydrogen and biofuels.

While the EU remains committed to the Green New Deal and the 2035 ICE ban, the fluctuating regulatory landscape creates uncertainty for zero-emission CV manufacturers. European battery manufacturers face growing competition from state-backed Chinese multinationals like FinDreams and CATL. The EU’s forthcoming battery passport initiative, set to launch in 2027, may provide European firms with a competitive edge by enforcing stricter environmental and transparency standards on imported batteries.

As Europe navigates economic stagnation and geopolitical tensions, the future of fleet electrification remains uncertain. Whether battery-electric, hydrogen, or alternative fuels will ultimately dominate remains to be seen.

Ursula von der Leyen, President of the EU Commission

*The European Automobile Manufacturers’ Association (ACEA) represents the 16 major Europe-based car, van, truck and bus makers: BMW Group, DAF Trucks, Daimler Truck, Ferrari, Ford of Europe, Honda Motor Europe, Hyundai Motor Europe, Iveco Group, Jaguar Land Rover, Mercedes-Benz, Renault Group, Stellantis, Toyota Motor Europe, Volkswagen Group, Volvo Cars, and Volvo Group. ACEA’s Bus and Coach division brings together Europe’s five main bus and coach manufacturers: Daimler Truck, Iveco Group, MAN, Scania, and the Volvo Group.